Quick answer

Wireless taxes and fees in the US typically add anywhere from the high teens to the high 20s percent on top of your base plan price, depending on your state and carrier. Some of those charges go to the government. Others go straight to the carrier — even if they're listed in the "taxes and fees" section of your bill.

Some prepaid carriers advertise all-in pricing with taxes included, but it's not universal — always check the plan terms before comparing totals.

Visual summary created with NotebookLM · Research and analysis by SwitchNinja Staff.

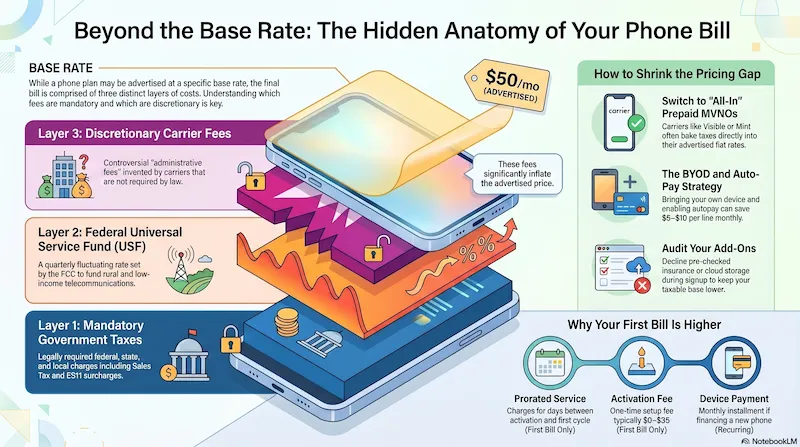

Your bill is actually three separate stacks

Think of it like a restaurant bill. The menu price is the base meal. Then comes the tax. Then a service charge. Then an "administrative processing fee" the restaurant added themselves. Your phone bill works the same way — three distinct layers, only one of which is actually required by law.

Layer 1 — Government taxes (mandatory)

These go to federal, state, and local governments. Carriers are legally required to collect them.

Federal and state sales taxes, telecom excise taxes, E911 surcharges, and state universal service contributions. The exact amount varies by ZIP code — state wireless tax burdens differ significantly. Your carrier and plan type can affect which taxes apply, but the underlying government rates are outside your control.

Layer 2 — Federal Universal Service Fund (USF)

Federally mandated but the rate fluctuates every quarter.

The USF funds telecommunications for rural areas, schools (E-Rate program), and low-income households (Lifeline program). The contribution factor — which determines how much carriers pass on to customers — is set quarterly by the FCC and has trended upward over time. Because it's percentage-based, it grows when your overall charges grow.

Layer 3 — Carrier fees (discretionary — this is the controversial part)

These are not taxes. They go to the carrier, not the government.

Administrative fees, regulatory cost recovery fees, network access fees — these are charges the carrier invented and can raise at any time without changing the advertised plan price. They are often listed right next to real government taxes on your bill, which makes them look official. They aren't. Carriers can and do increase these fees without technically "raising plan prices."

⚠ The labeling problem

Carrier-added fees are often listed in the same section as mandatory government taxes, with similarly official-sounding names. Most customers assume everything in that section goes to the government. Much of it doesn't. A "Regulatory Recovery Fee" is a company charge. An "Administrative Fee" is company revenue. The bill layout can make the distinction hard to spot.

Why the first bill is always the worst

The first statement after signing up is almost always the most alarming. That's because it stacks multiple one-time charges with a full month of service:

| Charge | What it is | Recurring? |

|---|---|---|

| Prorated service charge | Days of service from activation to billing cycle start | First bill only |

| Full month of service | First full billing cycle charged in advance | Every month |

| Activation fee | One-time setup fee (typically $0–$35; often waived during promos or for online orders) | First bill only |

| Device payment | Monthly installment if you financed your phone | Every month until paid off |

| Add-on services | Insurance, cloud storage, protection plans added at signup | Every month until cancelled |

All of the above then get taxes and carrier fees applied on top — which is why the first bill can look dramatically higher than the monthly rate you expected.

Why prepaid MVNOs often charge exactly what they advertise

Some prepaid MVNOs advertise all-in pricing where taxes and fees are baked into the flat rate. Visible is the clearest example — their advertised price is the total price. Other MVNOs like Mint Mobile and Tello typically add taxes at checkout, so the final amount varies by state. Always check the plan's fine print before assuming "taxes included."

T-Mobile has marketed tax-inclusive pricing on some flagship postpaid plans, though not across all products. Verizon and AT&T generally advertise pre-tax pricing — the final number depends on your state, city, and number of lines.

How to reduce the gap

Switch to a prepaid MVNO with all-in pricing

Mint, Visible, Tello, and others include taxes in their flat rates. What you see is what you pay. Still on a big-three plan? Compare T-Mobile vs AT&T →

Bring your own unlocked phone (BYOD)

Eliminates device payment line items, upgrade fees, and keeps your taxable base lower.

Set up autopay and paperless billing

Most carriers require both to unlock the advertised price. Without autopay, you typically pay $5–$10 more per line per month.

Audit add-ons at signup

Insurance, cloud storage, and device protection plans are often pre-checked during signup. Decline what you don't need — they add up fast and get taxed on top of everything else.

Ask for the "out-the-door" total before switching

When comparing carriers, always ask for the total monthly cost for your exact number of lines and ZIP code — not the base rate. That's the only number worth comparing.

Frequently asked questions

Why is my phone bill higher than the advertised price?▼

The advertised plan price is the base rate before government taxes, regulatory surcharges, and carrier-added fees. These extras commonly add 15–25% or more to your total bill, depending on your state, city, and carrier.

Are all fees on my phone bill actually taxes?▼

No. Government-mandated taxes are required by law, but carriers also add their own administrative and regulatory recovery fees that are not taxes — even though they often appear in the same section of your bill. These carrier fees go to the company, not the government.

Why is my first phone bill so high?▼

The first bill often includes prorated charges from your activation date, a full month of service, activation or upgrade fees, and any add-ons from signup. These all stack together, making the first statement much higher than the recurring monthly total.

Which carriers include taxes and fees in the advertised price?▼

Many prepaid MVNOs (like Mint Mobile, Visible, and Tello) advertise all-in pricing where taxes and fees are included. Most major postpaid carriers (Verizon, AT&T, T-Mobile) show a base plan price before taxes and fees, though T-Mobile has marketed tax-inclusive pricing on some plans.

⚡ The Bottom Line

The advertised price is the floor. Compare three numbers — not one.

1. Base plan price — what the carrier advertises

2. Estimated taxes and fees — ask for your ZIP code total

3. Device payment cost — if you're financing a phone

Add those three together and you have a real monthly total instead of a marketing headline. If that total is higher than you'd like, see our guide on how to lower your phone bill →

Want carriers that include taxes in the advertised price? Read our Visible review, Mint Mobile review, and Tello review.