Quick answer

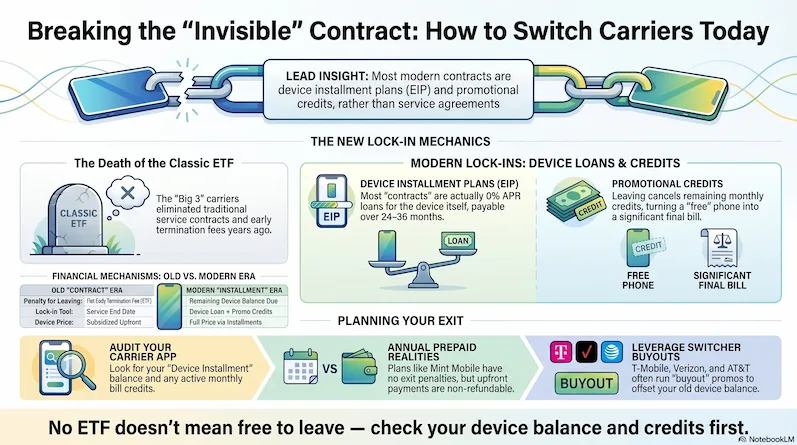

AT&T, Verizon, and T-Mobile no longer use traditional early termination fees on most consumer postpaid plans. There is no service contract to cancel. What most people have instead is a device installment plan — a loan for the phone itself — or promotional credits tied to staying with the carrier.

Leaving doesn't trigger a service penalty. But your remaining device balance typically becomes due on your final bill when you port out, and any promotional credits you were receiving stop when the line closes. The financial impact can be substantial — it just works differently than a classic ETF.

Infographic generated via NotebookLM from official carrier sources. Analysis by SwitchNinja Staff.

What an ETF actually was

Early termination fees were penalties built into two-year service contracts — the standard model before roughly 2015. When you signed a two-year contract to get a subsidized iPhone or Android, the carrier recovered that device subsidy through monthly service revenue over the contract term. If you left early, the ETF — typically starting around $175–$350 and often decreasing monthly as the contract progressed — was how the carrier recouped what remained.

T-Mobile launched the Un-carrier movement in 2013 and began moving consumers off two-year contracts. AT&T and Verizon followed within a couple of years. Today, most consumer postpaid plans at the major carriers no longer use traditional two-year service contracts or ETFs. The contract era is largely over — but a new form of lock-in replaced it.

| Old ETF Era (pre-2015) | Modern Installment Era | |

|---|---|---|

| Service agreement | 2-year service contract | Month-to-month |

| Penalty for leaving | ETF — up to $350 | None — but device balance accelerates |

| Device pricing | Subsidized upfront ($199–$299) | Full price via 36-mo installment |

| Lock-in mechanism | Contract end date | Device balance + promo credits |

What you're probably in today

Three things create the "I can't leave" feeling that people mistake for a contract:

Device installment plan (EIP)

You're paying for the phone in monthly installments at 0% APR — typically over 36 months at AT&T and Verizon, or 24 months at T-Mobile. This is a loan, not a contract. There's no penalty for leaving — but the remaining balance is typically accelerated to your final bill. Leave 18 months into a 36-month plan on a $1,000 phone and you might see $500 on your last bill.

How to check: Open your carrier's app → select your line → look for "Device Installment," "Device Payment," or "EIP." If there's a remaining balance listed, this is what you owe.

Promotional credits

When carriers advertise "get an iPhone 16 for free" or "save $800 when you switch," those discounts are usually delivered as monthly bill credits over 24–36 months — not an upfront price cut. When you cancel or port out your line, the credits stop. The remaining credits you haven't collected yet are simply gone.

One important distinction: paying off your device early while keeping the line active doesn't always end the credits — many promotions continue as long as the line stays active and meets the offer terms. It's porting out or canceling the line that triggers the cutoff.

How to check: Look at your monthly bill for line credits, trade-in credits, or promotional discounts. Multiply the monthly credit by the months remaining. That's the future savings you're giving up if you leave.

Annual prepaid plan (Mint Mobile, etc.)

Carriers like Mint Mobile offer deep discounts for paying 12 months upfront — but those payments are generally non-refundable after the return window (typically a few days from purchase). If you leave two months in, you don't get the remaining 10 months back. There's no penalty or ETF; you've just prepaid for service you won't use.

How to check: Look at your original purchase confirmation. If you paid for a year upfront, the unused months are already spent.

What it actually costs to leave

These three costs work differently — it's important not to lump them together:

| Cost type | What it means | Cash out of pocket? |

|---|---|---|

| Remaining device balance | The lump-sum payoff on your phone loan — hits your final bill when you port out | Yes — owed to old carrier |

| Lost promotional credits | Future bill credits that stop when the line closes — not money owed, but savings forfeited | No — opportunity cost only |

| Unused prepaid months | Already-paid service you won't use — non-refundable after the return window | No — sunk cost |

Timing tip

Your current carrier may also bill you for the full final billing cycle, not just the days you used. Most postpaid carriers don't prorate the last month's service fee. Factor this into your timing if you're close to a billing cycle renewal.

3 ways to get out

💸 Option 1 — Best if you want a new phone

Use a switcher buyout deal

Many carriers reimburse your remaining device balance when you switch over — usually as bill credits over 24–36 months or a prepaid card. You'll typically need to port your number, keep a new line active, and sometimes trade in your old phone. Read the fine print before assuming any specific offer applies — reimbursement timelines and eligible devices vary.

The math to run

Old balance + lost promo credits vs. new carrier buyout + monthly savings. If the buyout covers your balance and the new plan saves $30+/month, the switch pays for itself quickly. Can you switch if you owe money? →

🔓 Option 2 — Best if you're close to paying off

Pay off the balance, then BYOD to a cheaper carrier

If you're 6–8 months from the end of your installment plan, paying it off early and bringing your phone to an MVNO ($15–$35/month) is often the cleanest move. Paying off a $200 balance to save $40/month breaks even in 5 months — after that it's pure savings, often $400–$500 a year.

Before you go BYOD

Confirm your phone is unlocked and compatible with the new carrier's network. Most carriers have a free IMEI checker. How BYOD works →

⏳ Option 3 — Best if you're deep in promo credits

Wait out the remaining credit window

If you'd be forfeiting $600+ in remaining credits, the math usually favors waiting. Divide the credits you'd lose by your monthly savings at the new carrier — if the break-even is over 18 months, wait; if it's under 12, the switch may still make sense.

One thing to keep in mind

Promo deals that look like "free phones" are often really 36-month bill credits on a plan at full price. If you're unhappy with your plan, the "free phone" may be costing you far more in inflated plan costs than you're saving in credits. Why free phones aren't really free →

Step-by-step: how to leave

Check your device payoff balance

Log into your carrier app and find "Device Payoff Amount" — this is the lump sum, not the remaining monthly payments. That's what will appear on your final bill.

Add up any promotional credits you're receiving

Look at your bill for monthly line credits, trade-in credits, or switch credits. Multiply the total monthly credit by the months remaining. That's the true cost of leaving before the promo ends.

Compare your true switching cost vs. plan savings

Find a new plan that fits your usage. Calculate monthly savings vs. current plan. Divide your total exit cost by those monthly savings to get your break-even point in months.

Check if your phone is unlocked — or can be

iPhone: Settings → General → About → Carrier Lock. Android: varies by model. Unlock timing varies by carrier: AT&T and T-Mobile typically require the full balance to be paid before unlocking. Verizon generally auto-unlocks devices around 60 days after purchase — even while still on an installment plan — so Verizon users may not need to pay off the phone first. If you're using a buyout deal, plan for the unlock to happen after the balance clears, which may take a few days to process.

Get your account number and transfer PIN — don't cancel first

Log into your current carrier account or call to get your account number and transfer PIN. Do NOT cancel before porting — canceling first can cost you your phone number permanently. Porting to the new carrier closes the old account automatically. How to port your number →

Activate the new carrier, then handle the final bill

Complete the switch. Watch for a final bill from your old carrier — it will include any remaining device balance. If you negotiated a buyout with the new carrier, submit your final bill per their instructions to trigger the reimbursement.

Frequently asked questions

Do phone carriers still charge early termination fees?▼

For most consumer postpaid plans — yes. The major carriers (AT&T, Verizon, T-Mobile) have moved away from traditional early termination fees on consumer plans, which are now month-to-month with no service contract. The financial obligation you may have is a device installment balance, which is not the same thing as an ETF — but it can still appear as a lump sum on your final bill if you leave before paying it off.

What is the difference between an ETF and a device installment plan?▼

An ETF (early termination fee) was a penalty for canceling a service contract before its end date — typically starting around $175–$350 and decreasing monthly as the contract progressed. A device installment plan (EIP) is a loan for the phone itself — you owe the remaining balance because you haven't finished paying for the device. There's no penalty for leaving, but the unpaid device balance typically becomes due on your final bill.

What happens to my phone installment balance if I switch carriers?▼

The remaining installment balance is typically accelerated — meaning it becomes due on your final bill rather than continuing as monthly payments. Any promotional credits tied to keeping the device on that carrier also stop. You still legally owe the balance; switching carriers doesn't erase it.

How do I know if I'm in a contract or on an installment plan?▼

Log into your carrier's app and look for "Device Installment" or "Device Payment Plan" under your line details. If you see a remaining balance with a monthly payment amount, you're on an installment plan, not a contract. If there's no device balance listed, you own your phone outright and have no financial obligation beyond the current month's plan cost.

Does Mint Mobile have an early termination fee?▼

Mint Mobile doesn't have an ETF — but its annual plan is generally non-refundable after the return window (typically a few days from purchase). If you pay for 12 months upfront and decide to leave two months in, you don't get the unused months back. This is soft lock-in, not a traditional contract, but the financial result is similar in the early months of an annual term.

⚡ The Bottom Line

You're almost certainly not in a contract — but you may still owe money.

True ETFs haven't existed at the major carriers for years. What keeps people stuck is the combination of device installment balances and promotional credits — both real financial obligations, just packaged differently than a traditional contract.

Before you switch, add up your payoff balance and uncollected credits. Divide that by your monthly savings at the new carrier. If the break-even is under 12 months, switching usually makes sense. If it's 24+ months, it may be worth waiting — unless the new carrier's buyout covers the difference. Weighing where to go next? See Verizon vs T-Mobile or browse our carrier reviews before you commit.