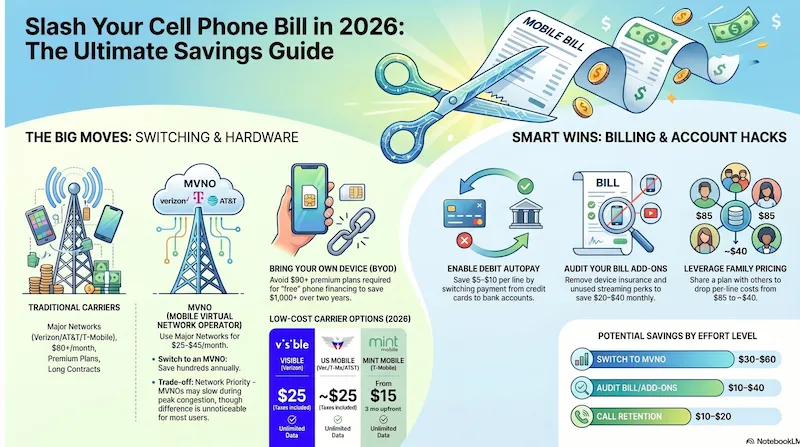

Quick answer — savings by effort level

- $30–60/mo savings: Switch to an MVNO or prepaid carrier on the same network

- $10–40/mo savings: Remove device insurance, unused add-ons, and premium tier perks

- $5–10/line savings: Enable AutoPay with a debit card or bank account

- $25–45/mo savings: Pay off your phone and switch to a BYOD plan

- $10–20/mo savings: Call retention and threaten to leave (works ~50% of the time)

Infographic generated via NotebookLM from official carrier policy sources. Analysis by SwitchNinja Staff.

1. Switch carriers — the biggest lever

If you're on a postpaid plan with Verizon, AT&T, or T-Mobile and paying $75–100/month for a single line, you can almost certainly get the same coverage for $25–45/month through an MVNO — a smaller carrier that runs on the same network.

| Carrier | Network | Unlimited price | Taxes included? |

|---|---|---|---|

| Visible | Verizon | $25/mo | Yes |

| US Mobile Starter | Verizon / T-Mobile / AT&T | ~$25/mo | Yes |

| Mint Mobile | T-Mobile | From $15/mo* | No |

| Cricket | AT&T | $45/mo | Yes |

| Tello | T-Mobile | From $10/mo | No |

*Mint pricing reflects 12-month upfront payment. Month-to-month rates are higher. Prices verified May 2026.

The tradeoff: MVNOs generally have lower network priority than postpaid plans during congestion — meaning your speeds may slow in crowded areas during peak hours. For most people in suburban or rural areas, the difference is unnoticeable. If you're in a dense city and need consistent speeds, a mid-tier MVNO like Visible+ or US Mobile Premium gives you priority data at a still-significant discount. Learn more about deprioritization →

2. Enable AutoPay with a debit card — easiest $5–10/line

All three major carriers offer a discount for AutoPay and paperless billing. In 2026, most require a bank account or debit card — not a credit card — to qualify for the full amount.

| Carrier | AutoPay discount | Payment method required |

|---|---|---|

| AT&T | $10/line (bank) · $5/line (debit) | Bank account (ACH) = $10; debit card = $5; most credit cards = no discount |

| Verizon | Up to $10/line | Bank/debit card on most plans |

| T-Mobile | $5/line | Bank/debit card for full discount |

For a family of four on AT&T: that's $40/month — nearly $500/year — just for switching your payment method. Takes about 5 minutes in the app.

3. Stop financing your phone through your carrier

Carrier "free phone" deals aren't free — they're financed over 24–36 months through monthly bill credits, and they almost always require you to stay on a more expensive premium plan for the full term. BYOD (bring your own device) removes that lock-in entirely.

BYOD on Visible

$25/mo

Unlimited on Verizon's network. No device payment. Leave anytime.

Financed iPhone on Verizon

$85+/mo

Premium plan required. 36-month commitment. Early exit = balance due immediately.

Over two years, the BYOD path often saves $1,000–1,500 compared to financing through a major carrier — even accounting for the full cost of buying an unlocked phone.

When carrier financing makes sense: If you were already planning to stay on a premium plan and a trade-in offer brings the device cost to near zero, financing can be worthwhile. The math only works if you don't switch carriers for the full term. See the full trade-in math →

4. Add lines — family plans dramatically cut per-line cost

Carriers price per-line costs to reward multi-line accounts. A single line that costs $85/month can drop to $40–50/line on a 4-line family plan. You don't need to be related — any group of people can share a family plan.

| Carrier | 1 line | 4 lines (per line) | Savings/line |

|---|---|---|---|

| T-Mobile Experience More | $85 | ~$43–50 | ~$35–42 |

| AT&T Extra 2.0 | $70 | ~$35–40 | ~$30–35 |

| Verizon Unlimited Plus | $70 | ~$35–45 | ~$40–45 |

Even on MVNOs, family pricing helps. US Mobile's multi-line pricing and Mint Mobile's family plans reduce per-line cost further, though the absolute savings are smaller since the base prices are already low.

5. Audit your bill — what you're paying for but probably don't need

| Feature | Typical cost | Why to cut it |

|---|---|---|

| Device insurance / protection plan | $11–19/line/mo | Deductibles run $99–299. On older phones, the deductible exceeds the phone's value. Many credit cards include cell phone protection if you pay the bill with the card. |

| Premium unlimited tier | $10–20/mo extra | Most people use under 20–30GB/month and never hit the priority data ceiling on mid-tier plans. Check your actual usage before paying for 100GB+ priority. |

| Bundled streaming services | $5–15/mo value | Many people already pay for Netflix, Hulu, or Apple TV+ separately. If you're double-paying, downgrade your plan and keep your existing subscriptions — it's often cheaper. |

| International roaming add-ons | $10–20/mo | If you travel internationally less than once a year, cut the monthly add-on. Buy a local eSIM for your trip instead — typically $10–20 for 10GB, one time. |

| Tablet / watch lines you don't use | $10–25/line/mo | These lines don't cancel automatically when you switch your phone line. Check every line on your account and cancel any you use primarily on Wi-Fi. |

| Early upgrade / Next Up fees | $5–10/mo | You're paying monthly for the option to upgrade early — a perk that benefits the carrier far more than you. Most people keep phones 2–3 years. |

6. Call retention — works about half the time

If you don't want to switch carriers, calling and threatening to leave is the next best option. It works roughly 50% of the time and typically yields $10–20/month in temporary loyalty credits for 6–12 months.

What to say

Call customer service and ask for the retention or cancellation department. Then say something like:

"I've been a customer for X years and I'm looking at Visible for $25/month on the same Verizon network. Is there anything you can do to lower my bill before I make the switch?"

This works best if your phones are fully paid off, you've been a customer for 2+ years, and you can name a specific competitor with a lower price. The rep can often apply a loyalty credit on the spot. If they can't, ask when your contract or promo period ends and call back then.

⚡ SwitchNinja take

Start with your bill. Then decide if you're switching or staying.

Open your last bill and look for three things: device insurance, any add-ons you didn't consciously choose, and whether AutoPay with a debit card is enabled. Just fixing those can free up $20–40/month without touching your plan.

If your phone is paid off and you're still on a $75–100 postpaid plan, the math on switching to an MVNO is almost always decisive. You're paying a premium for the carrier's brand, not their network — the network is the same either way.

Comparing your current carrier to cheaper options? See our AT&T vs T-Mobile comparison or read the T-Mobile review.